Europe’s automotive edge at risk as China’s value-added output surges past the EU

For decades, the European automotive supply industry has sustained a robust trade surplus, being an undisputed engine of global value creation. Today the engine is stalling.

The most striking shift is in production value. China has expanded its capacity at such a pace that it now produces roughly twice as much in value-added terms as the EU. This surge, alongside rising imports from lower-cost hubs is actively cutting the trade surplus that once underpinned Europe’s industrial strength. Simultaneously, exports to key, traditional markets like the United Kingdom and the United States have begun to decline.

Taken together, these trends point to a rapid erosion of Europe’s role as a global powerhouse in traditional automotive components. To remain competitive, the EU must implement targeted measures to preserve production capacity, address structural cost disadvantages, and support investment in domestic manufacturing. Without decisive action, thousands of jobs will be lost, and European companies will face the relocation of production outside the region.

Benjamin Krieger, Secretary General

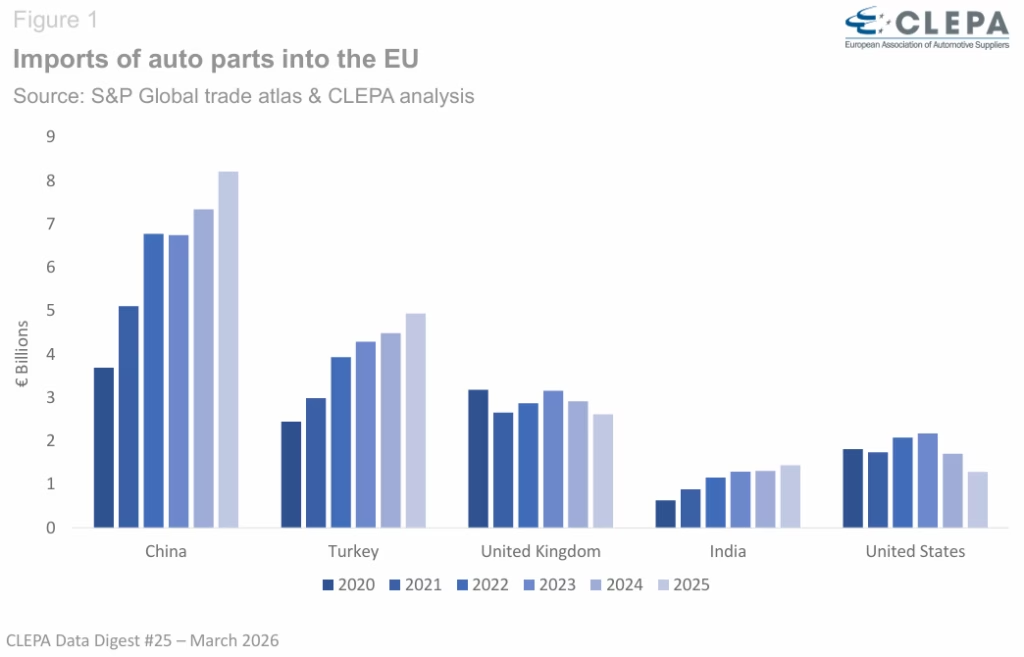

Chinese imports now account for nearly one-third of the EU market, while Turkey emerges as a fast-growing exporter

Imports from China continue to dominate the EU market for traditional automotive components, growing by 12% compared to last year. Chinese imports now exceed €8 billion, representing around 30% of total EU imports in this components category.

At the same time, sourcing patterns are shifting toward newer regional hubs. Imports from Turkey have doubled over the past five years, now reaching approximately €5 billion. Imports from the United Kingdom, Japan and South Korea remain broadly similar in scale, each supplying around €2.5 billion worth of components to the 2025 EU market.

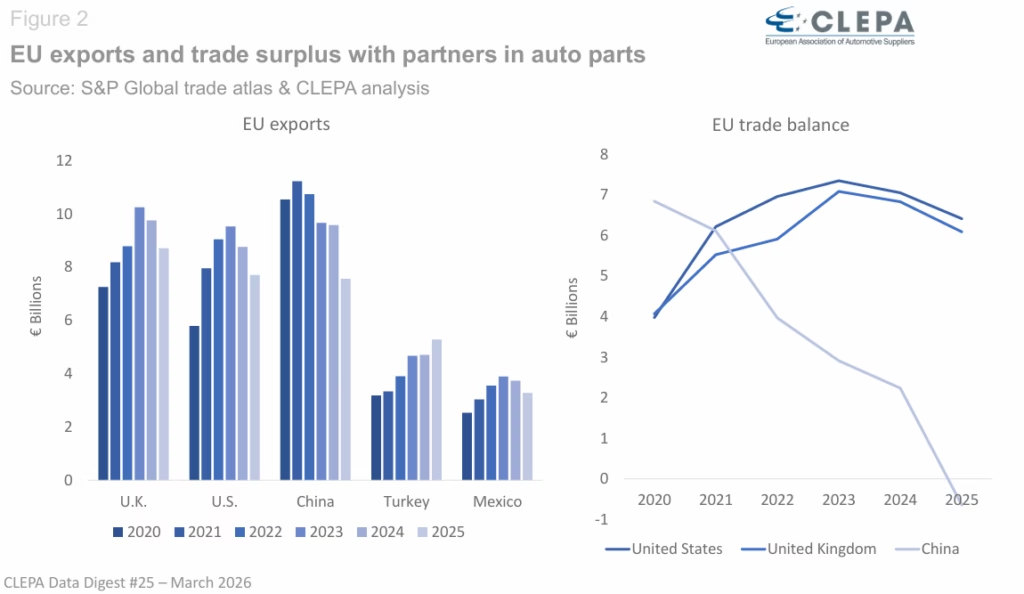

The EU’s trade surplus shrinks as exports to China fall below imports

Exports of automotive components have deteriorated significantly over the past years, leading to a declining trade surplus of 30% since 2021, falling from €28.7 billion to €20 billion. The primary driver of this decline is a fundamental shift in trade relationship with China.

EU exports of automotive components to China have fallen below import levels. In 2025, exports to China reached only €7.5 billion, while imports exceeded €8 billion. Over the past five years, EU exports to China have declined by roughly €3 billion, reversing what had previously been a strong surplus relationship. As a result, the EU now records a trade deficit with China of around €650 million in traditional automotive components.

Relations with traditional trade partners such as the UK and the US, which had been compensating for the declining trade surplus with China, are now deteriorating as well.

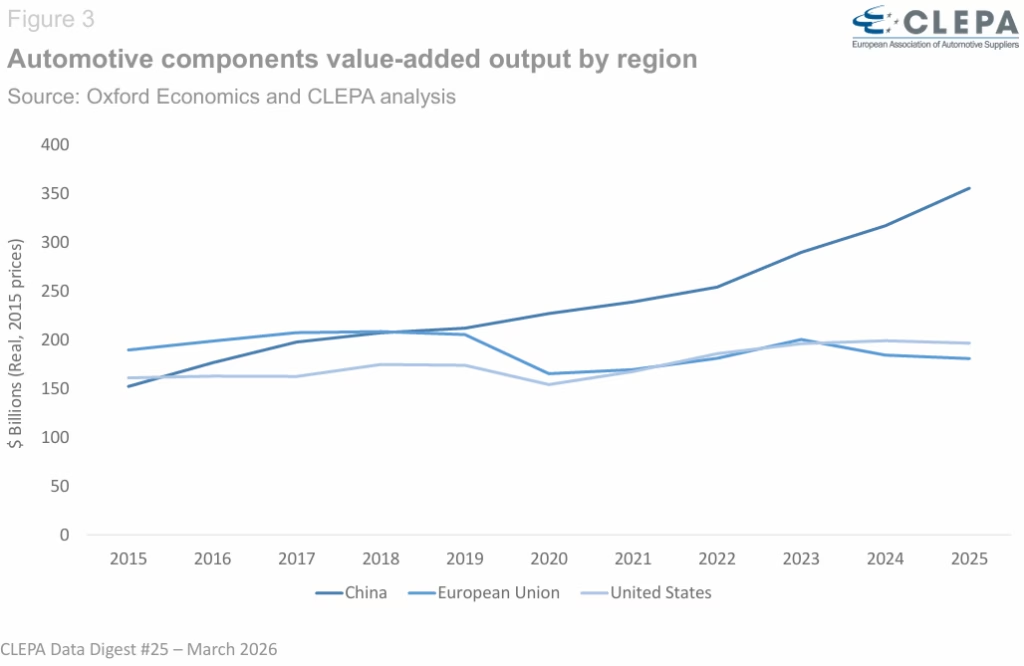

The EU loses its global lead in automotive component production as China strengthens its dominance

The EU was the world’s largest producer of automotive components in value-added terms until 2018.

Since then, production trends have diverged. China and the United States expanded output, while EU production declined. Between 2018 and 2025, China’s value-added output increased by around 40%, exceeding $380 billion, reflecting the rapid expansion of its automotive supply chain. Over the same period, US production grew by roughly 11%.

By contrast, EU output fell by about 15%, dropping to around $180 billion. This means that China now produces more than double the value of the EU in this sector.

Contact CLEPA Communications Team at communications@clepa.be